The Escalating Burden of Residential Service Charges: A Structural Analysis of Housing Affordability

The landscape of urban living across Western economies is currently undergoing a silent but profound transformation. For decades, the acquisition of a leasehold property or an apartment within a managed complex was viewed as a strategic entry point into the real estate market. However, a systemic surge in service charges and communal maintenance fees is fundamentally altering the financial viability of this asset class. What began as incremental adjustments for inflation has evolved into a full-scale affordability crisis, threatening the solvency of households and the stability of the secondary housing market. This report examines the multi-faceted drivers of these rising costs and the broader economic implications for property owners who find themselves at the mercy of complex management structures.

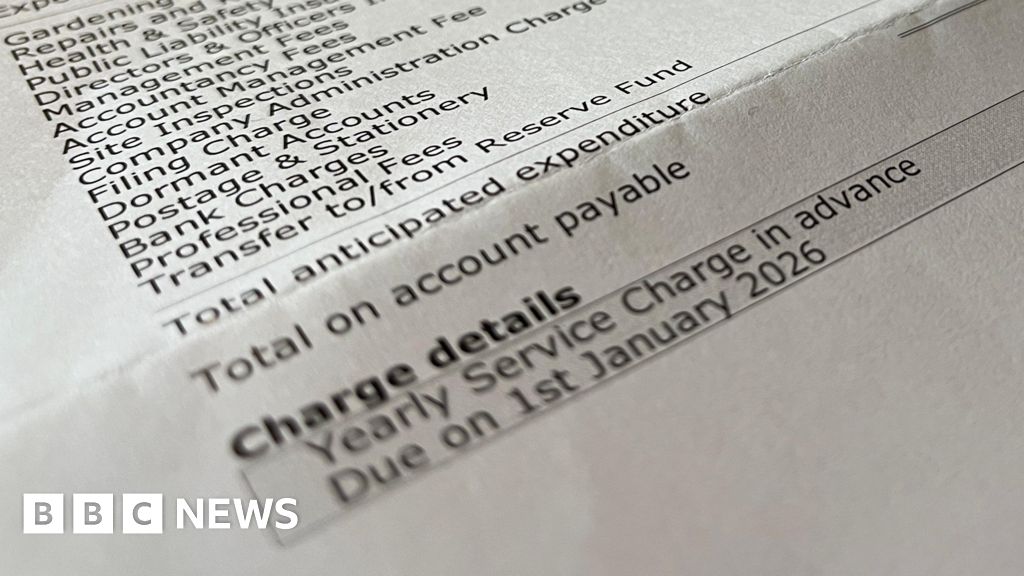

The current predicament is characterized by a significant decoupling of management fees from the actual quality of services provided. Across major metropolitan hubs, homeowners are reporting annual increases that far outpace Consumer Price Index (CPI) benchmarks. These charges, which cover everything from concierge services and landscaping to structural insurance and emergency repairs, have become a primary source of financial anxiety. As operational costs balloon, the resulting fiscal pressure is forcing many residents to reconsider the long-term sustainability of their investments, often discovering that the very homes intended to build equity are instead eroding their disposable income and savings.

The Convergence of Regulatory Compliance and Insurance Volatility

A primary driver behind the aggressive escalation of building charges is the evolving regulatory environment, particularly regarding fire safety and structural integrity. In the wake of high-profile disasters and subsequent legislative overhauls,such as the Building Safety Act in the United Kingdom and similar safety mandates across European jurisdictions,management companies have been forced to undertake extensive audits and remediation works. While these measures are essential for resident safety, the financial burden of compliance has been shifted almost exclusively onto the leaseholders. The cost of “waking watches,” cladding removal, and the installation of advanced fire suppression systems has introduced five-figure levies that many households are ill-equipped to meet.

Compounding this regulatory pressure is a hardening insurance market. Insurers have significantly reassessed the risk profiles of multi-occupancy buildings, leading to premium hikes that frequently exceed 100% year-on-year. In many instances, the lack of transparency in how these insurance contracts are brokered has led to allegations of excessive commissions and “kickbacks” between brokers and management agents. For the resident, this manifests as an unavoidable, non-negotiable expense that offers no tangible improvement in daily living standards but significantly increases the monthly cost of occupancy. The result is a structural inflation that is effectively “baked into” the property’s overhead, regardless of the individual owner’s financial circumstances.

The Opacity of Management Governance and Fiduciary Oversight

The relationship between residents and managing agents is often characterized by an inherent power imbalance and a lack of granular transparency. Professional management firms operate with significant autonomy, often entering into long-term service contracts with third-party vendors without a competitive tendering process. This lack of market tension frequently leads to inflated costs for routine maintenance, such as cleaning, lift servicing, and general repairs. For the layperson, deciphering a 50-page annual accounts statement is a daunting task, and the legal mechanisms required to challenge these costs,such as First-tier Tribunals,are often prohibitively expensive and time-consuming.

Furthermore, the “reserve fund” or “sinking fund” mechanism, intended to smooth out the costs of major works over several years, is frequently mismanaged or underfunded. When significant structural issues arise, residents are often hit with “special assessments” or “major works bills” that require immediate payment of substantial sums. This unpredictability is perhaps the most damaging aspect of the current system. Unlike a traditional mortgage, where payments are relatively predictable, building charges represent a volatile variable that can spike without warning, undermining the financial planning of even the most diligent homeowners. This fiscal volatility is increasingly being recognized by financial institutions, leading to stricter lending criteria for properties with high or poorly managed service charges.

Systemic Implications for Liquidity and Asset Devaluation

The financial impact of rising charges extends far beyond the immediate monthly budget; it is beginning to exert downward pressure on property valuations. In a rational market, as the cost of holding an asset increases, the capital value of that asset should decrease to maintain a comparable yield or total cost of ownership. We are now observing a phenomenon where apartments in high-charge buildings remain on the market for extended periods, often requiring significant price reductions to attract buyers. Prospective purchasers are increasingly wary of the “hidden costs” associated with leasehold properties, leading to a flight toward freehold assets where the owner retains greater control over expenditures.

This shift has created a class of “mortgage prisoners”—homeowners who cannot afford to stay due to rising charges but cannot afford to sell because the high fees have diminished the attractiveness of their property to the point of negative equity. For the broader economy, this reduces labor mobility and stifles the “stepping stone” function of the apartment market. When a significant portion of a household’s income is redirected from consumption or investment into administrative overhead and insurance premiums, the overall economic multiplier effect is diminished. The erosion of home equity also impacts the long-term retirement security of a generation that has relied on property ownership as its primary financial safety net.

Strategic Analysis: The Path Toward Reform

The current crisis in building charges is not merely a byproduct of inflation; it is a symptom of a systemic failure in the governance of multi-unit residential properties. For the market to regain stability, a fundamental shift toward transparency and accountability is required. This necessitates legislative intervention to cap management commissions, mandate competitive tendering for all major contracts, and provide residents with more accessible avenues for dispute resolution. The “Right to Manage” processes must be streamlined to allow homeowners to wrest control from negligent or exploitative management firms, fostering a more competitive environment for property services.

Ultimately, the sustainability of high-density urban living depends on the predictability of its costs. As Western cities continue to densify, the model of residential management must evolve from a profit-extraction mechanism for third-party agents into a transparent service utility for residents. Failure to address these structural imbalances will likely lead to a continued stagnation in the apartment sector, deeper social inequality, and a persistent drag on the wider housing market. Professionalizing the sector and aligning the interests of managers with those of the residents they serve is no longer just a consumer rights issue; it is an economic imperative.

{kind=link}